One lawsuit can wipe out years of profit. As a general contractor, you face liability exposure every single day — on the jobsite, in your contracts, and even after a project wraps up. Learning how to protect a general contractor from liability isn't just about having the right insurance policy. It's about combining coverage, contract language, and compliance practices into a system that holds up when things go wrong. This guide covers exactly that: practical, specific strategies you can use starting today to keep your business protected.

Table of Contents

- Key takeaways

- Protect your general contractor business with the right insurance

- Contractual strategies that limit your liability exposure

- Insurance compliance verification on every project

- Risk transfer and safety practices that go beyond paperwork

- My take on where contractors actually get hurt

- How Snapqualify helps you stay ahead of liability risks

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Insurance is your first line of defense | General liability coverage protects against bodily injury, property damage, and legal defense costs on every project. |

| Endorsements matter more than COIs | Certificates of insurance are summaries only; the actual policy endorsements determine what coverage you have. |

| Tailor indemnity clauses by state | Broad indemnity language may be void in certain states, so your contracts must match local rules to hold up in court. |

| Verify subcontractor insurance actively | Reviewing a COI is not enough; contact the insurer to confirm active, adequate coverage before work starts. |

| Safety documentation reduces claims | Keeping records of safety protocols gives you the factual narrative needed to defend against claims or litigation. |

Protect your general contractor business with the right insurance

General liability insurance is the foundation of contractor risk management. Without it, a single injury claim or property damage dispute could cost you more than your annual revenue. Here's what a solid policy actually covers and where the gaps are:

- Third-party bodily injury: Medical costs and legal fees if someone other than your employee is hurt on the job

- Third-party property damage: Repair or replacement costs if your crew damages a client's property

- Legal defense costs: Attorney fees and court costs even if a claim turns out to be groundless

- Completed operations coverage: Protection for claims that arise after a project is finished, such as a roof leak discovered months later

General liability coverage does not cover employee injuries (that's workers' comp territory) or most professional errors. Know those exclusions before you assume you're covered.

On pricing, the average annual cost for construction businesses sits around $1,351, though your actual premium depends on payroll size, the type of work you do, and your location.

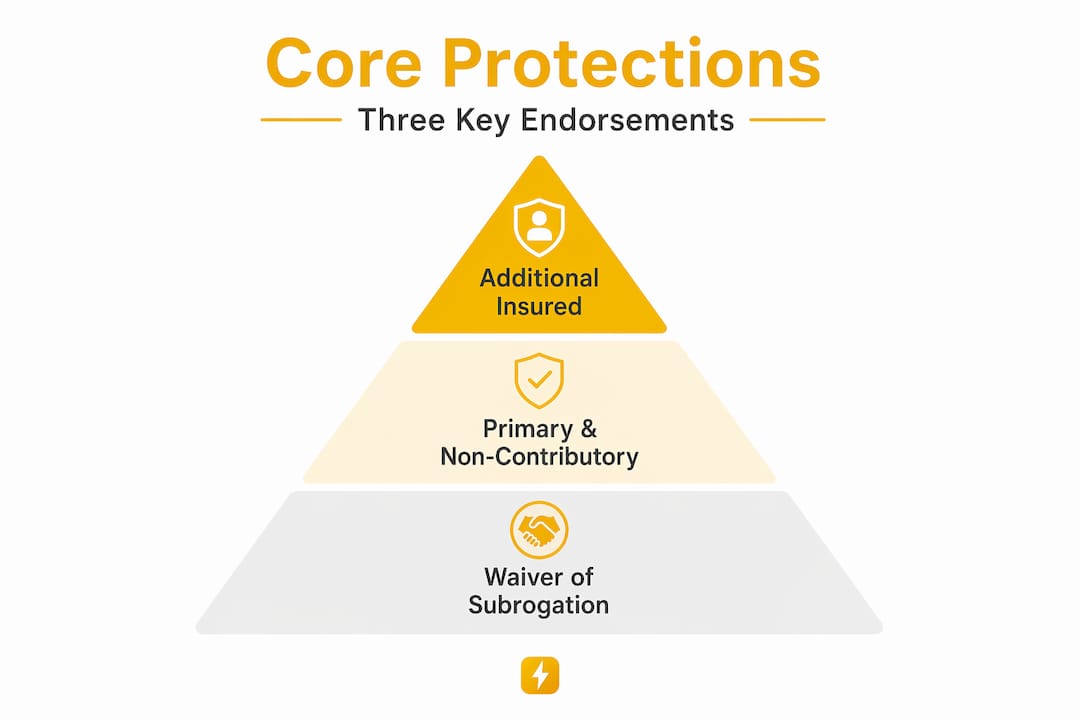

Beyond the base policy, three endorsements work together to give you real protection on multi-party projects. The endorsement trio of Additional Insured, Primary and Non-Contributory, and Waiver of Subrogation defines who pays first in a claim and blocks an insurer from suing another party to recover costs. These endorsements typically add $25 to $200 per endorsement depending on how they're scheduled. That's a small price for the protection they deliver.

Pro Tip: When an owner or GC asks to be added as an additional insured, request a copy of the actual endorsement form. Owners and GCs often assume that seeing their name on a COI means full coverage, but the COI is only a summary.

Contractual strategies that limit your liability exposure

Your contract is your second layer of defense. Every clause you negotiate before a project starts is protection you won't have to fight for later. Here are the most important contractual elements to address, in order of priority:

-

Indemnity clauses: Require subcontractors to indemnify you for losses arising from their own negligence. Be specific about what's covered and from whose negligence. Broad indemnity language that tries to shift liability for your negligence to a sub may not hold up. Indemnity enforceability varies significantly by state, so a clause that works in Texas may be void in Virginia.

-

Additional insured requirements: Your contract should require subs to name you as an additional insured on their general liability policies. Spell out the specific form number when possible, not just the concept.

-

Primary and non-contributory language: Without this clause, a sub's insurer can argue that your policy should share the loss equally. Requiring primary and non-contributory status means their policy pays first, every time.

-

Waiver of subrogation: This clause prevents a sub's insurer from suing you to recover money it paid out. Get it in writing and confirm the endorsement is in place before work starts, not after a claim is filed.

-

State-specific review: Have a construction attorney review your template contracts for the states where you operate. Anti-indemnity statutes vary widely, and courts will enforce what's in your contract even if you didn't fully understand it when you signed.

Pro Tip: Don't just send a standard contract template and assume it covers you. Review your subcontractor agreements at least once a year with a local construction attorney. A one-hour legal review is far cheaper than one uncovered claim.

Understanding common subcontractor contract disputes before they happen is one of the smartest investments you can make in your contracting business.

Insurance compliance verification on every project

Getting the right language in your contracts only works if you actually confirm that your subs carry the coverage they promised. This is where most GCs fall short.

Here's a practical compliance checklist to run through before any subcontractor starts work:

- Check the business name on the COI: Confirm the named insured matches the legal entity you contracted with, not a related company or a DBA that may not be covered under that policy

- Verify policy dates: Active today does not mean active next month. Policies lapse, and you won't always get notified

- Confirm products and completed operations coverage: This protects you after the job is done, not just during construction

- Request actual endorsement documents: A COI is informational only and does not itself grant coverage rights. The endorsement form is what matters in a claim

- Call the insurer or agent to confirm: Verbal assurances or COIs can be out of date the moment a policy lapses or gets modified

Use a document control system to store COIs and endorsement PDFs linked to each project. When a claim arises, you need those files immediately, not after a panicked search through email archives.

| Verification step | Why it matters |

|---|---|

| Match legal entity names | Ensures the right company is actually covered under the policy |

| Confirm coverage dates | Policies can lapse mid-project without your knowledge |

| Request endorsement forms | COIs don't grant rights; endorsements do |

| Contact insurer directly | Confirms policy is active and limits are accurate |

| Store documents by project | Speeds up claims response and proves compliance |

Risk transfer and safety practices that go beyond paperwork

Contracts and insurance handle the financial side of liability. But they don't protect you from a regulatory finding or a jury that decides your jobsite was unsafe. Real protection requires combining paperwork with practice.

- Document your safety protocols in writing before every project starts. A written safety plan signals to courts, regulators, and insurers that you take compliance seriously

- Statutory safety obligations like New York Labor Law §240 impose strict liability on GCs for elevation-related injuries regardless of worker negligence. Contract protections cannot override statutory duties

- For federal or government work, compliance documentation is critical. Faithfully following government instructions and recording that compliance gives you a defense that contract language alone cannot provide

- Train your crew regularly and keep records of that training. If a claim goes to litigation, you want evidence showing an ongoing safety culture, not just a poster on a wall

Your contract can transfer risk. Your insurance can fund a defense. But your safety program is what prevents the incident that triggers both.

Look into subcontractor default insurance as an additional layer of risk transfer, especially on larger projects where a sub's failure could cascade into serious GC liability.

My take on where contractors actually get hurt

I've reviewed dozens of liability situations, and the pattern is almost always the same. Contractors think they're covered because they have a policy and a signed contract. They're not looking at the details.

The biggest blind spot I see is the endorsement gap. A sub names the GC as additional insured on the COI, but the actual endorsement is a blanket form with a vague project description that doesn't match the jobsite address or the contracting entity's legal name. When a claim hits, the insurer disputes coverage. That gap costs GCs real money, and it was entirely preventable.

The second issue is indemnity assumptions. I've seen contractors use the same contract template in five different states without realizing that three of those states have anti-indemnity statutes that void the clause they're counting on. Contract language that looks airtight in one jurisdiction is legally unenforceable in another.

The fix isn't complicated. Get your endorsement documents, not just the COI. Check the entity names. Review your contracts by state. Track compliance proactively, not reactively. And build a real safety culture because a documented safety program is one of the strongest liability defenses you have.

— Colin

How Snapqualify helps you stay ahead of liability risks

Managing compliance across multiple subcontractors and projects is a lot to track manually. Snapqualify was built to help trade contractors and GCs work smarter by screening clients before problems start.

With Snapqualify's intake forms and AI-driven SnapScore, you get a fast read on client reliability before you commit time and resources to a bid. Knowing which clients are likely to cause payment disputes, scope creep, or compliance headaches means you can make better decisions upfront. Your client and project data stays protected through Snapqualify's secure data practices. If you want to reduce the risk that starts before the contract is even signed, Snapqualify is worth a close look.

FAQ

What does general liability insurance cover for contractors?

General liability insurance covers third-party bodily injury, property damage, legal defense costs, and completed operations claims. It does not cover employee injuries or most professional errors.

Can a COI alone prove my subcontractor is insured?

No. A certificate of insurance is informational only and does not grant coverage rights. You must request the actual endorsement forms and confirm the policy is active by contacting the insurer directly.

Are indemnity clauses always enforceable in contractor agreements?

Not always. Indemnity enforceability varies by state, and broad clauses that attempt to shift liability for your own negligence may be void under local anti-indemnity statutes. Have a construction attorney review your contracts for each state where you operate.

What are the most important insurance endorsements for a GC?

The three most critical endorsements are Additional Insured, Primary and Non-Contributory, and Waiver of Subrogation. Together, they define who pays first and prevent insurers from pursuing you to recover claim costs.

How can I protect myself from liability after a project is complete?

Require completed operations coverage in every subcontractor policy. Keep project records, safety documentation, and endorsement files for at least the duration of your state's statute of limitations for construction claims.